At Mobile World Congress in Barcelona last week, phone manufacturers showed off new devices without naming prices. Not because they hadn't decided. Because they couldn't. Memory costs were shifting too fast. Xiaomi announced the 17 at 999 euros on stage. "The price they announced on stage is not the price they will see the phone at," IDC's Francisco Jeronimo told CNET. Retail would land 100 euros higher.

Three thousand kilometers east, in Amsterdam, a Dutch court had just ordered a formal investigation into Nexperia, the chipmaker whose components sit inside the headlights, airbag systems, and anti-lock brakes of cars built by Honda, Volkswagen, and Mercedes-Benz. The court upheld the suspension of CEO Zhang Xuezheng and found that a conflict of interest had been "handled without due care." Nexperia's Chinese parent, Wingtech, responded with $8 billion in compensation threats.

Two events in two cities. One about phones nobody can price. The other about chips nobody can move. They look unrelated.

They aren't.

China's consumer electronics industry is caught in a vise. One jaw is AI's appetite for memory, which has tripled RAM costs and redirected 70% of global DRAM production toward data centers. The other is geopolitical. Governments in The Hague and Beijing are physically severing supply chains that moved components between continents for decades. The mid-tier smartphone brands that powered China's mobile revolution? Caught in the middle. Bleeding cash.

The Breakdown

- DRAM contract prices up 90-95% in Q1 2026, driving the biggest smartphone shipment decline in a decade

- Nexperia split into two rival companies after Dutch government seized control, disrupting auto chip supplies for Honda, VW, and Mercedes

- Sub-$100 smartphones may become permanently uneconomical, cutting mobile access for hundreds of millions

- Memory makers profit while 190,000+ small electronics companies fight for scraps at hourly-shifting prices

The price tag that changes by the hour

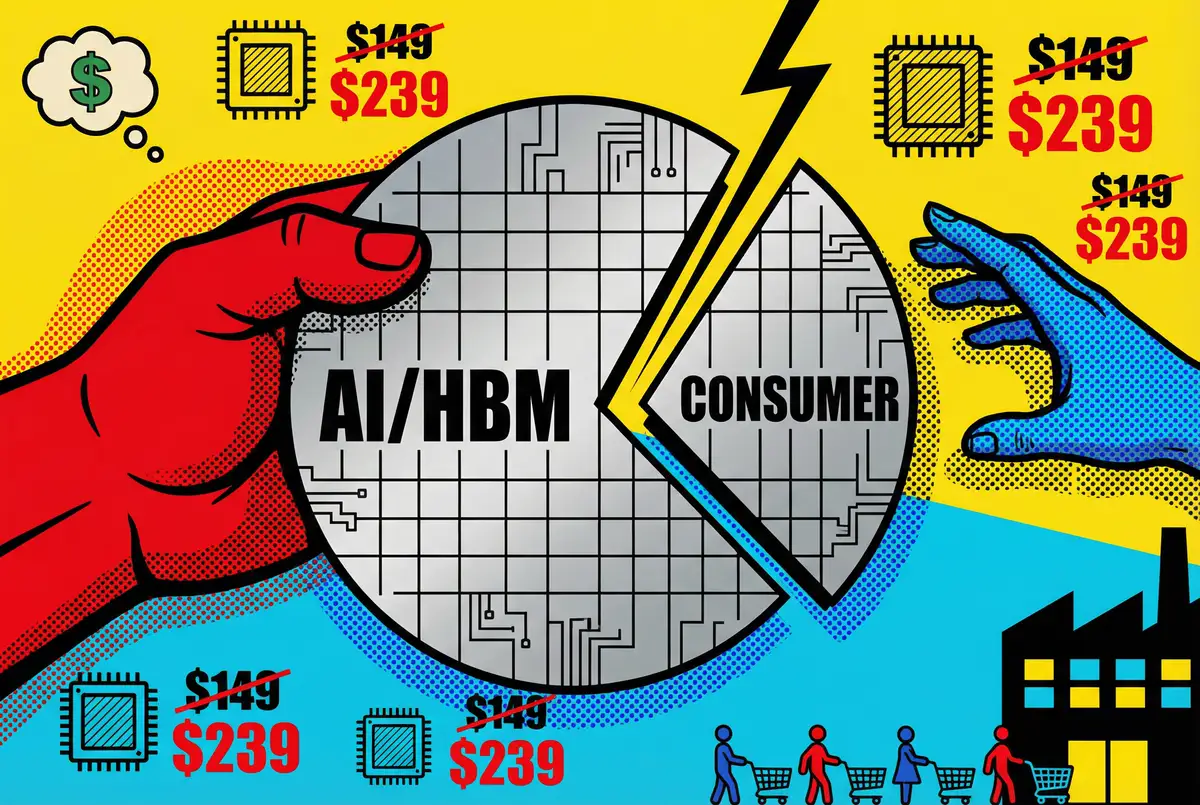

Late last year, Samsung, SK Hynix, and Micron started pulling production capacity away from conventional DRAM. The destination: high-bandwidth memory for AI servers. Shortage has been building since. But since January, conditions have gotten worse faster than IDC's worst-case scenarios predicted just months ago.

TrendForce revised its Q1 2026 DRAM contract price forecast to a 90-95% quarter-over-quarter increase, nearly double earlier projections. NAND flash climbed 55-60% in the same period. A DigiTimes report from early March described DRAM pricing shifting on an hourly basis, with smaller buyers receiving higher quotes within minutes if they couldn't commit upfront payment.

That's not a typo. Hourly.

The market has split cleanly in two. Roughly 100 top-tier buyers, cloud providers, automakers, Apple, Samsung, hold enough purchasing power to secure priority allocation. The other 190,000-plus small and mid-size electronics companies? They fight over whatever's left.

IDC's latest forecast puts global smartphone shipments at 1.12 billion units in 2026, a 12.9% plunge from the 1.26 billion shipped last year. The biggest single-year decline in over a decade. Counterpoint pegged it at 12%. Average selling prices will rise 14% to a record $523. And the sub-$100 smartphone, the category that connected hundreds of millions of people in Africa, India, and Southeast Asia to the internet, may become "permanently uneconomical," according to IDC's Nabila Popal.

HP disclosed that DRAM now accounts for 35% of its PC bill of materials. Up from 15-18% just one quarter earlier. Phison's CEO warned in February that consumer electronics companies could face bankruptcy by year's end. Nothing CEO Carl Pei put it in terms his customers would understand. "The 'more specs for less money' model that many value brands were built on is no longer sustainable in 2026."

This is the first jaw of the vise. It squeezes hardest in China.

Nexperia splits in two, and so does the supply chain

The second jaw looks different but bites the same place.

On March 3, Nexperia's Dutch headquarters disabled the corporate accounts of every employee in China. Office 365, gone. SAP, gone. The order-to-production workflow for customer-supplied wafers, interrupted. Nexperia China said in a client letter that the action "significantly disrupted" operations and triggered an emergency response.

Beijing's commerce ministry fired back within days. The Dutch side "must bear full responsibility should these measures trigger another crisis in the global semiconductor industry and its supply chains," Xinhua reported Saturday.

The account lockout is only the latest fracture in a breakup that started in September 2025, when the Dutch government invoked emergency powers to seize control of Nexperia, citing national security concerns over Wingtech's ownership. A Dutch court suspended Zhang, transferred Wingtech's voting rights to a trustee, and launched a formal investigation.

Beijing retaliated with export controls on Nexperia's China-made chips. Honda halted production in Mexico. Volkswagen scrambled for alternatives.

A temporary truce reopened exports after Trump and Xi met in late October. But Nexperia's Dutch headquarters never resumed wafer shipments to the Dongguan plant, which historically handled 70% of the company's total output. The Chinese unit declared itself independent of European management. Both sides accused the other of bad faith. The company that produced over 110 billion chips per year was now two companies, each missing what the other had.

Nexperia China claims it delivered 11 billion chips to 800 clients since mid-October despite the constraints. A 14% production drop. The unit began qualifying domestic wafer suppliers, a process expected to finish by mid-2026. But you can't rebuild a qualified automotive-grade supply chain in six months. These aren't generic components. Each chip controls a specific function in a specific vehicle system, and requalification takes time that production lines don't have.

Wingtech is threatening $8 billion in compensation under a bilateral investment treaty, with the arbitration window opening April 15. The Dutch side is accelerating a $300 million investment in Malaysian capacity to shift 90% of production out of China. Both sides are building parallel supply chains. Neither will be cheaper.

Where the jaws meet

The two crises converge here, and you see the structural shift in the numbers.

China's smartphone makers built their business on two foundations. Cheap memory made budget phones possible. Global supply chains made the whole thing run. Wafers left Hamburg, crossed to Dongguan, came back as finished chips to Stuttgart. Cheap and fast. Both cracked in the same quarter.

Stay ahead of the curve

Strategic AI news from San Francisco. No hype, no "AI will change everything" throat clearing. Just what moved, who won, and why it matters. Daily at 6am PST.

No spam. Unsubscribe anytime.

Memory costs are eating margins from above. Xiaomi, Oppo, Vivo, Honor. They all run on thin margins, thinnest in the sub-1,000 yuan phones that powered a decade of mobile growth across Asia. New models already cost 100 to 600 yuan more than last year's equivalents. Some midrange hikes hit 20%. Brands are reportedly preparing another round of increases.

And the supply chains that held it all together are fracturing along national borders. Nexperia is the most visible case, but the pattern runs deeper. Each new export control or entity list designation throws sand into machinery built to move fast, not to take hits.

On February 27, Meizu quit. The company suspended all self-developed hardware for new phones. Every smartphone model vanished from its Taobao store. Only accessories remain. That's what happens when the math stops working.

The anxiety across Shenzhen is palpable. Market share is concentrating fast toward brands with enough cash and supplier relationships to ride this out. Apple owns more than 70% of China's market above 8,000 yuan. It launched the iPhone 17e at 4,449. Subsidies bring it under 4,000. Samsung swallowed a $100 hit on the Galaxy S26. Bumped base storage to 256GB, stacked trade-in offers. Held the price.

Xiaomi can probably ride this out. It has a war chest and an EV business pulling in a quarter of revenue. If you're a smaller player with thin cash flow, you're competing for hourly-priced memory against Apple's procurement team. That's not a competition. It's a countdown.

Who pays for the structural reset

IDC calls this "a structural reset of the entire market." That phrase is doing a lot of work, but it's accurate.

Winners are easy to spot. Samsung, SK Hynix, and Micron are printing money. Samsung's Q4 2025 operating profit tripled year-over-year on memory sales alone. Apple locked in long-term supply deals. The worst swings don't touch it. Huawei's domestic supply chain gives it an edge no other Chinese brand can match.

The losers are harder to count because many of them will simply stop existing. Counterpoint sees the sub-$200 segment losing a fifth of its volume. Africa and the Middle East run on sub-$150 phones. IDC projects shipments there falling more than 20%. Chinese consumers are holding onto phones longer, too. The average replacement cycle stretched from 28 months to 33. The second-hand phone market will grow. That's cold comfort for manufacturers who need to sell new devices to stay alive.

And the 190,000 small and mid-size electronics companies fighting for memory scraps? Many are already cutting demand forecasts in what DigiTimes called a "cut losses to survive" strategy. If enough of them pull back simultaneously, the tight market could flip to oversupply. But that's not a comfort to the companies that won't last long enough to see the correction.

The phone with no price tag

At MWC, Unihertz showed off the Titan 2 Elite without a finalized price. Before this shortage, phone prices were locked weeks or months before launch. Now manufacturers can't commit until the last possible moment because the memory they need for assembly might cost more by the time they finish building.

At 7:02 PM on March 3 in Dongguan, a Nexperia employee's Office 365 account went dark. By Friday, the Chinese unit said most operations had resumed. "Basic production" was continuing. That's the language of damage control, not stability.

Two small moments in a structural rearrangement that won't easily reverse. The cheap phone that brought a billion people online was built on abundant memory and fluid supply chains. One broke because AI pays more. The other broke because governments decided the risk of integration outweighed the efficiency. Neither force is temporary. Neither is reversible on any timeline that matters to the companies bleeding cash right now.

The vise doesn't open from the inside.

Frequently Asked Questions

Why are memory chip prices rising so fast in 2026?

Samsung, SK Hynix, and Micron shifted production capacity from conventional DRAM to high-bandwidth memory for AI servers. AI data centers pay more per chip, so manufacturers prioritize them. TrendForce reports Q1 2026 DRAM contract prices rose 90-95% quarter-over-quarter. Smaller buyers now receive price quotes that change within hours.

What happened to Nexperia and why does it matter?

The Dutch government seized control of Nexperia in September 2025 over national security concerns about its Chinese parent Wingtech. The company effectively split in two. Nexperia produces 110 billion chips per year for automotive systems. The breakup disrupted supplies for Honda, Volkswagen, and Mercedes-Benz, with Honda halting production in Mexico.

Which smartphone brands are most at risk?

Mid-tier Chinese brands operating on thin margins face the greatest threat. Meizu already suspended all phone hardware. Brands in the sub-1,000 yuan segment are hiking prices 100-600 yuan per model. Xiaomi can likely survive thanks to its cash reserves and EV revenue. Smaller players competing against Apple's procurement power face a countdown.

How does the memory shortage affect consumers in developing countries?

IDC projects smartphone shipments in Africa and the Middle East will drop more than 20%. The sub-$100 phone that connected hundreds of millions to the internet may become permanently uneconomical. Average selling prices globally are rising 14% to a record $523. Consumers in China are already holding phones 33 months instead of 28.

Could the memory market correct itself?

Possibly, but not soon enough for many companies. If enough small manufacturers cut orders simultaneously, the tight market could flip to oversupply. But that correction would come too late for companies already bleeding cash. The structural forces driving the shortage, AI demand and geopolitical supply chain fractures, are not temporary.

Related stories